Representative Stephen Lynch wants to create e-cash

Representative Stephen Lynch wants to create e-cash

Stablecoins, CBDCs, and e-cash: what's the difference?

Welcome back!

First off, it’s a big holiday weekend for many, so Happy Passover and Happy Easter to those celebrating!

As for this week’s newsletter, I wanted to focus on something I have been putting off for a while: stablecoins and central bank digital currencies. These two applications of crypto have dominated crypto policy discussions, and, recently, a new concept of e-cash has entered the arena.

I hope you enjoy, and see you next Sunday!

-Katja

Representative Stephen Lynch wants to create e-cash

In the world of crypto regulation, stablecoins and central bank digital currencies (CBDCs) have garnered the most attention. McKinsey highlighted this growing interest in non-traditional cryptocurrencies…

“The European Central Bank announced recently it was progressing its ‘digital euro’ project into a more detailed investigation phase. More than four-fifths of the world’s central banks are similarly engaged in pilots or other central bank digital currency (CBDC) activities. Concurrently, multiple private, stabilized cryptocurrencies—commonly known as stablecoins—have emerged outside of state-sponsored channels, as part of efforts designed to enhance liquidity and simplify settlement across the growing crypto ecosystem.”

Recently, Rep. Stephen Lynch (D-MA) introduced a new bill that would develop an electronic version of the dollar, creating what he termed “e-cash,” which creates a third category of crypto that the government may investigate.

Stablecoins

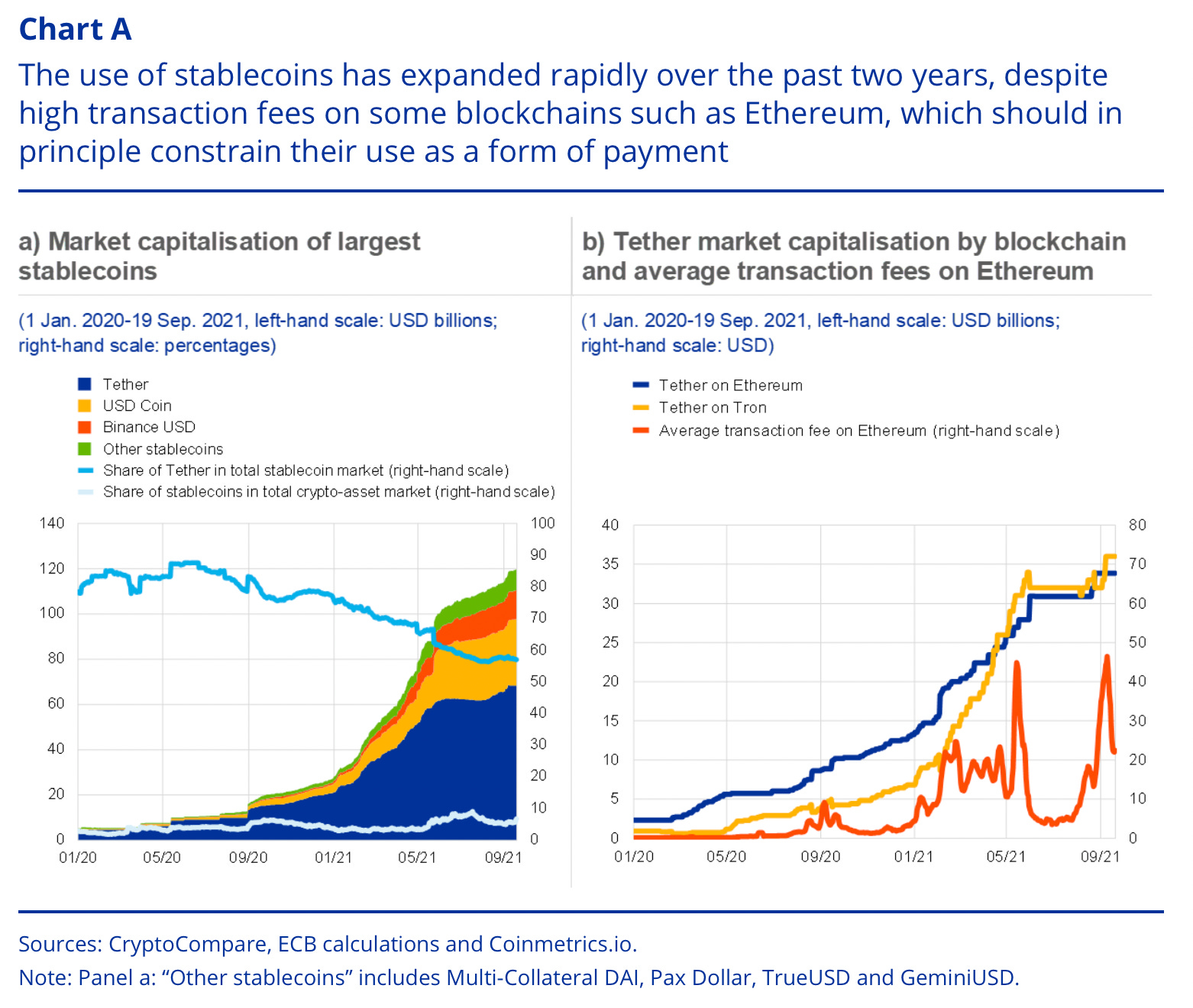

A stablecoin is a digital asset that is pegged to some reserve asset (like the US dollar). Having this backing allows stablecoins to avoid the volatility of traditional crypto while maintaining the benefits of the blockchain (fast transaction speed and low cost). Because of this, stablecoins can be viewed as a “bridge” between traditional fiat and digital assets.Their use cases continue to expand as blockchain technology develops, but right now, stablecoins are mainly used for trading or as collateral in decentralized finance (DeFi).

Stablecoins became one of the first and main areas of focus (in crypto) for the US government, so they get a decent amount of attention in Congress. Several weeks ago, I covered the House hearing on stablecoins, which mainly focused on the downside of stablecoins and explored a proposed federal regulatory framework for them.

CBDCs

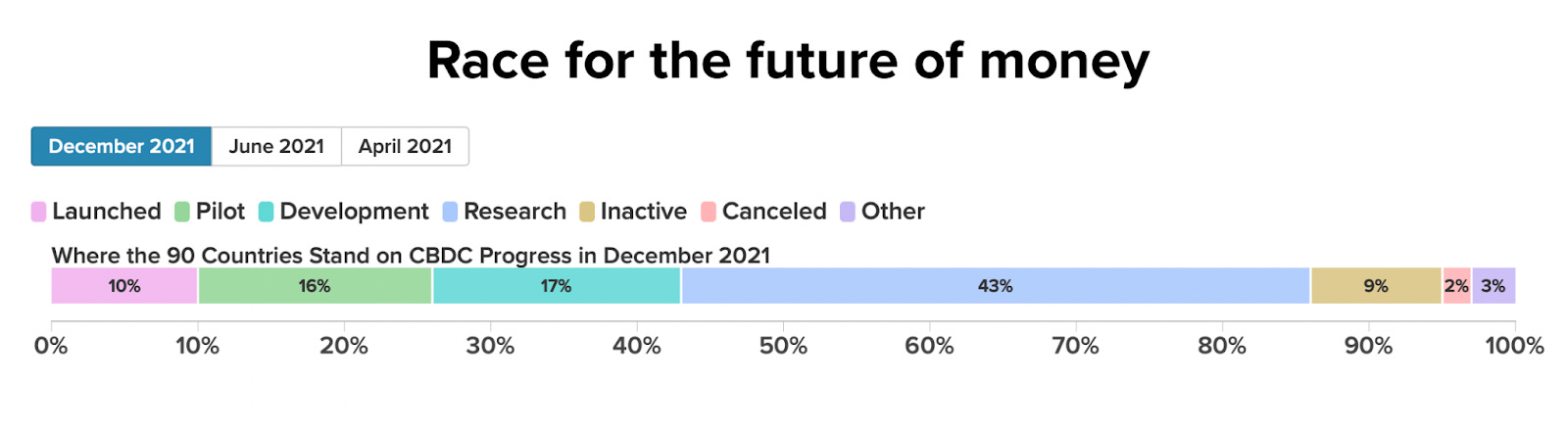

The rise in popularity of stablecoins has prompted central banks to start exploring their own digital assets called central bank digital currencies. CBDCs are exactly what they sound like: digital currency (crypto) that is issued by a central bank (the government) and pegged to that country’s fiat currency.

The interest in CBDCs probably stemmed from the potential impact of privately-issued stablecoins on financial stability and monetary policy. To no surprise, the government, alongside banks, doesn’t want something to usurp its power. However, other reasons for venturing into CBDCs include: increasing accessibility to the financial system and reducing payment frictions.

One of the main issues surrounding CBDCs is that governments seem to view them as more than just digital-native fiat. Some (I would argue the vast majority of) governments want to use CBDCs as programmable money in a way that could track consumer spending as well as restrict an individual’s funds. Just for context, China has banned crypto besides its government’s CBDC (eCNY - digital yuan), which should tell you something about its use case.

E-cash

Now, let's return to Rep. Lynch’s e-cash. As the bill discusses, the US Treasury would issue e-cash, instead of the US central bank (the Federal Reserve). It would also not use a centralized ledger (like most CBDCs) or a distributed ledger (like traditional crypto). CoinTelegraph reported,

“Rohan Grey, an assistant law professor at Willamette University’s College of Law who helped draft Lynch’s bill, said in an interview that the Fed doesn’t have the statutory authority to create a CBDC or the capacity to maintain the retail accounts that would be required for it. Instead, he described the digital dollar as something replicating the privacy, anonymity and transactional freedom reflecting the properties of physical cash.”

In theory, e-cash seems like a stablecoin and CBDC hybrid: it’s not fully outside the control of the government but does pose less privacy and surveillance threats to its users. In practice, e-cash doesn’t seem viable or realistic.

Individuals who use cryptocurrency (including stablecoins) do so because it gives them freedom, autonomy, and privacy. This promise behind crypto is what’s powering the movement away from banks and what’s allowing the bankless to find their place in a financial system. CBDCs and e-cash violate these principles, and will most likely not reach mass adoption.

Even outside of this, a central question remains: why create a new system controlled by the government that’s inconsistent with blockchain values, when stablecoins already exist and have shown their value proposition?

Because of this, I think the US is much more likely to go down the path of regulated stablecoins as opposed to developing a CBDC. Although e-cash is an interesting concept to add to the discussion, I also don’t see it gaining traction on the Hill.