Debunking common misconceptions around crypto

Debunking common misconceptions around crypto

What Senators Warren and Brown got wrong

Welcome back!

This week, Congress continued to discuss digital assets in an effort to figure out regulatory next steps. While basking in the glory of American politics during the ongoing hearings, it really started to bother me how some politicians are relentless in their fight against digital innovation.

However, I do understand the uneasy attitude some may feel about the new industry. Therefore, this week, I wanted to debunk common misconceptions about crypto to give it the fair evaluation it deserves.

Enjoy, and see you next Friday!

-Katja

Debunking common misconceptions around crypto: What Senators Warren and Brown got wrong

Senators Warren (D-MA) and Brown (D-OH) expressed some of the more “anti-crypto” sentiments during the last Senate hearing. Although I do not believe in the arguments they made, I think it is important to consider their points and look at the evidence.

Uses and users

If you watched the Super Bowl, you probably noticed crypto commercials from companies like Coinbase, FTX, and Crypto.com. You may have not thought twice about these ads, but Sen. Brown argued that they demonstrate how crypto companies are “desperate” to reach as many Americans as they can to maximize the company’s profits. He went further by saying: if crypto is simply a currency, why do you need to advertise it?

Sen. Warren extended this point by saying that stablecoins are supposed to represent the future of payment systems but are only used to lubricate the “shadiest part” of the crypto ecosystem.

This argument can be broken down into two main categories: crypto uses and risks. Although I’ve covered the benefits of crypto and blockchain before, I want to highlight and reiterate some central ideas.

The blockchain allows for faster speed, lower fees, and transparency in payment systems. These three core pillars contribute to some important use cases like sending remittances and alternative banking.

Sen. Brown said that he understands this appeal of crypto, but he doesn’t see stablecoins as anything but a speculative instrument, comparing this crypto era to the early 2000 dot com bubble. Because of this, he said that crypto isn’t the type of “inclusion” that Americans seek in financial institutions.

He brought up the unbanked in making that point, so let's consider why someone may not have a bank account. Under US laws, banks must follow Know Your Customer (KYC) regulations in order to establish someone’s legitimacy and identify their risk factors.

“Under KYC, clients must provide credentials that prove their identity and address. Verification credentials can include ID card verification, face verification, biometric verification, and/or document verification. For proof of address, utility bills are an example of acceptable documentation.

KYC is a critical process for determining customer risk and whether the customer can meet the institution’s requirements to use their services. It’s also a legal requirement to comply with Anti-Money Laundering (AML) laws. Financial institutions must ensure that clients are not engaging in criminal activities by using their services.”

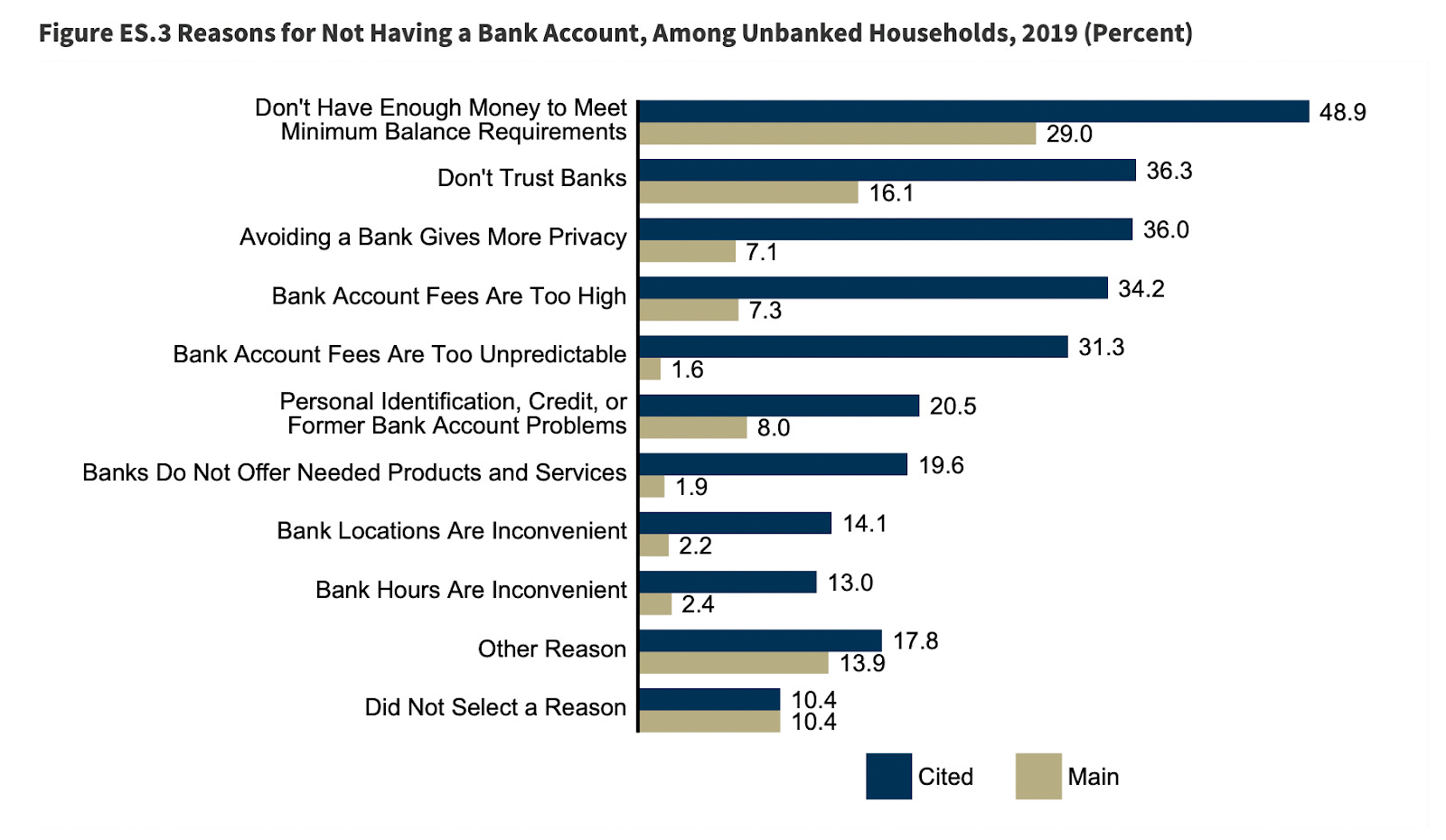

These requirements automatically filter out a portion of the population. In addition to this, the Federal Deposit Insurance Corporation (FDIC) conducted a survey in 2019 that focused on identifying further trends of the unbanked. The results from the survey showed that unbanked rates were higher among Black and Hispanic households as compared to White households.

FDIC also found that the main reason for not having a bank account is inability to meet minimum balance requirements. Other top reasons included distrust of banks, lack of privacy, and high fees.

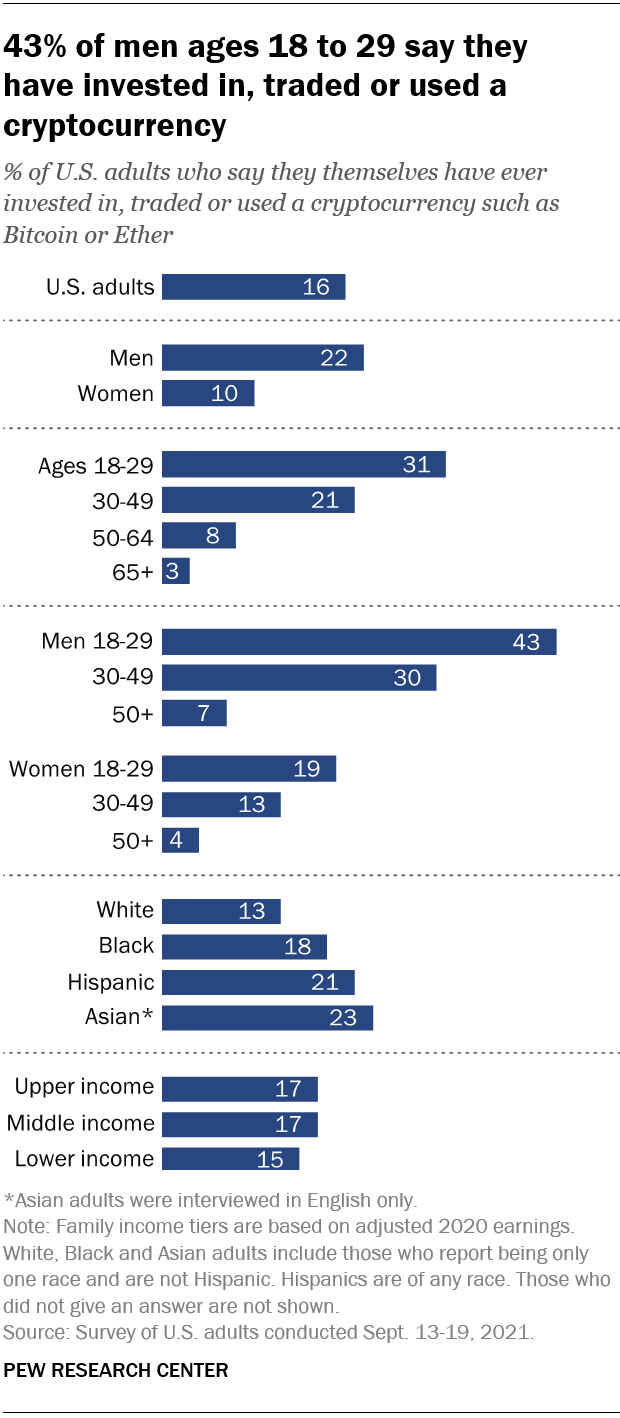

On the other hand, Pew Research conducted a study on crypto use, and found some interesting trends, including how Asian, Black and Hispanic adults are more likely than White adults to say they have ever invested in, traded or used a cryptocurrency.

At the intersection of these two studies, we can see that minority individuals are turning to crypto because banks are not able to meet their needs. This goes in direct contrast to what Sen. Brown suggested about how Americans do not want this type of “inclusion” in the crypto space.

In fact, crypto companies aren’t pushing this inclusion, they’re embracing the inherent inclusion the system is providing to individuals that the traditional financial system did not support.

Now, let's return to the crypto Super Bowl ads.

Some of these ads featured celebrities like LeBron James and Larry David and toyed around with the idea of hopping on the crypto wave so as to not miss out on this new social trend.

These crypto companies tried to create hype around cryptocurrencies. They didn’t mention more speculative markets like NFTs or talk about the more theoretical applications of blockchain as part of Web3. Overall, these commercials aimed to expand the adoption of crypto at the most basic level: by buying cryptocurrency.

Due to this, I want to re-consider Sen. Brown’s comment about advertising currency. He said that in his 40 years of watching the Super Bowl, he’s never once seen a commercial for the US dollar, implying that advertising currency is a ridiculous idea. If we look back at history, I would argue that, given the same technology existed at that time, the government would have gone to great lengths to advertise its first national currency to avoid the chaos following the Free Banking Era.

It may seem wild to use advertising for this purpose, but it’s the most efficient and effective tool for mass adoption. Besides this, crypto is not the same as traditional fiat currency. It’s new and revolutionary, and it requires a different approach (much like when the first national currency was created in 1863).

Risks

The PWG report covered a long list of risks, including loss of value (risks to users and stablecoin runs), payment system risks, and risks of scale (systemic risk and concentration of power). Both Senators had a heavy focus on these risks and pushed for the idea that the risks completely outweigh any potential benefits.

This rhetoric around crypto is very prevalent among politicians to the extent that the PWG report did not even have a section for the benefits of stablecoins. These risks are important to consider, especially in how they affect everyday investors. [I’ve talked about some risks surrounding crypto in a previous newsletter, if you want to read more about it.]

However, in considering the risks of crypto, we should also be evaluating the risks of current financial institutions. If we do that, we can see that many of the same risks apply to both systems. In addition to this, traditional financial institutions also pose another layer of risk that stems from human negligence or malfeasance (like fraud, self-dealing, insider trading, etc). This human-centered risk is at the core of what blockchain solves for by removing the human component from finance.

[This newsletter isn’t focused on evaluating the risks of traditional financial institutions, so if you want to read more about the topic, check out this article by Brian Brooks.]

Obviously picking between the two systems requires weighing the costs and benefits. However, trying to take down crypto for its risks while not recognizing its benefits or the risks posed by alternatives is too simplistic and does nothing to help the American people.

As Senator Toomey (R-PA) said during the hearing …

“Congress and regulators should remember that our mission is not to make it impossible for a financial institution to fail. It is not to make it impossible for an investor to lose money… It is, in my view, to ensure that investors are well-informed about the risks that they choose to take and to make sure if there is a financial institution that fails, it doesn’t have catastrophic systemic consequences.”

Senators Warren and Brown viewed stablecoins, and crypto more generally, through a very narrow lens. I discourage this type of outlook because it shuts down the productive discussion around what the government can do to minimize the risks while maintaining the benefits of crypto. We need such conversations because they’re the only way to solve serious issues and encourage innovation.